Why Permanent Capital Changes Everything About How You Underwrite

When you don't have an exit date, the spreadsheet stops being the answer. The quality of the business becomes everything.

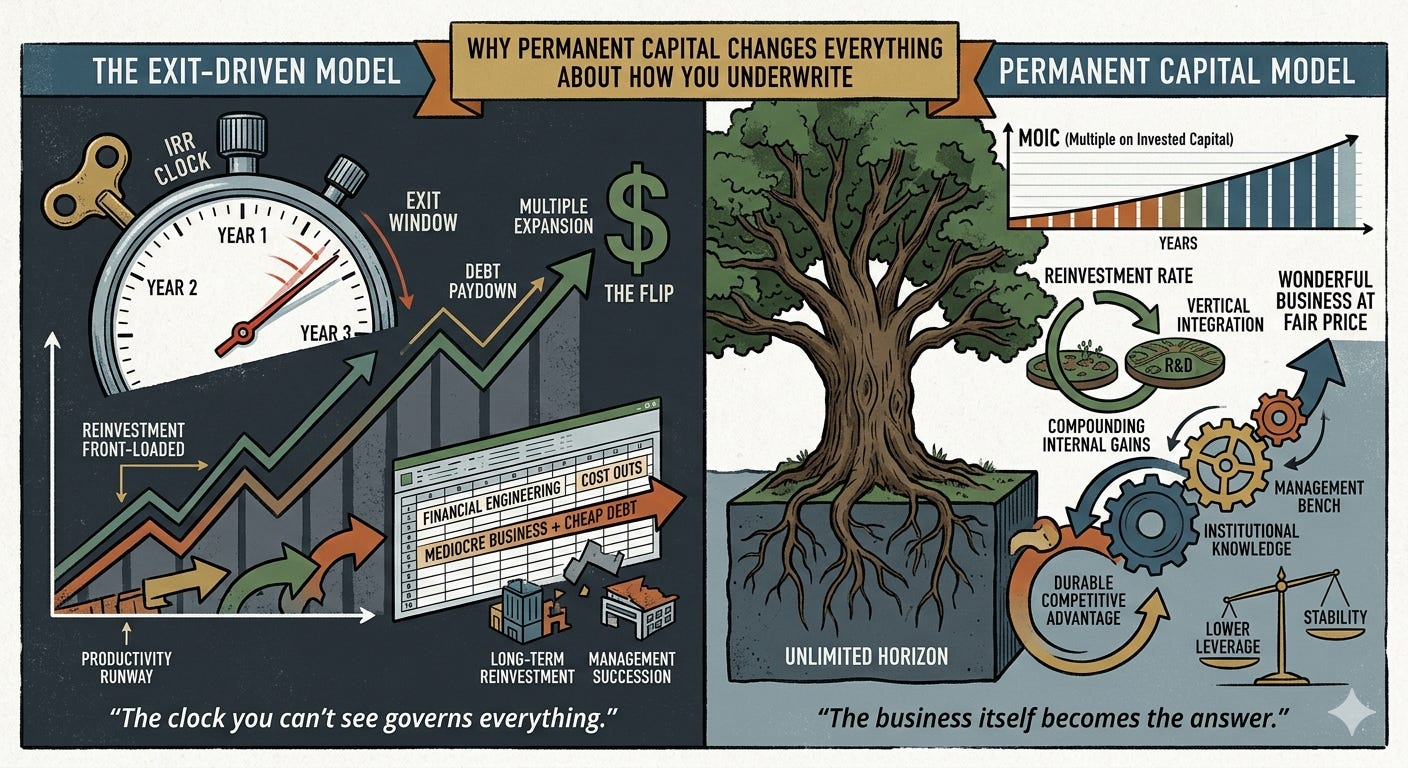

The clock you can’t see

The standard PE model has three acts. Act I: You buy a business at some multiple of EBITDA, usually with a meaningful portion of debt. Act II: You spend three to five years improving it; growing earnings, paying down the debt, tightening operations. Act III: You sell it, ideally at a higher multiple than you paid, into a market that’s receptive.

Everything in that model is governed by one number: IRR. And IRR has an inherent clock built in. The faster you get capital back, the better the return looks, almost regardless of what happens to the business afterward.

That clock creates a specific set of incentives. Some are good: discipline on entry price, urgency on value creation, a forcing function against complacency. But it also creates distortions the industry rarely says out loud.

The first is front-loading. Anything that pays off after the hold window is invisible to returns. A reinvestment that compounds beautifully in year seven is, to a year-five seller, just cash out the door for someone else’s benefit. And so it will typically not get made.

The second is that you stop underwriting the business and start underwriting the next buyer’s story. The equity narrative, the “platform,” the multiple of the day. Salability quietly becomes the strategy.

And the third is the part nobody wants to admit: a mediocre business, bought cheap, levered fully, and sold into a strong multiple market can produce an outstanding IRR. The quality of the underlying business is almost incidental to the outcome. A number of great track records are really products of a good multiple environment and cheap debt.

No exit, no excuses

Permanent capital removes the need for an exit. That’s the headline, and it’s the part people fixate on — the long horizon, no fund-life pressure, no forced sale into a bad market. But the more important half is the part that sounds like a downside. There’s no exit to bail you out.

In the flip model, a sale is the universal solvent. Mispriced the business? Sell it. Operational problems you can’t fix? Sell to someone who thinks they can. Cycle turning against you? Time the exit and move on. The transaction launders a lot of mistakes.

Take that away and every mistake stays on your own balance sheet (indefinitely). You are the buyer of last resort, and the buyer of last resort is you. There’s no next owner to inherit the problem and no clock that ends the accountability.

This is why “no exit” and “no excuses” are the same sentence. You don’t get to blame the hold period or the LP clock or the window closing. If the business is bad in year twelve, that traces back to a decision made in year one.

We find this brings clarity to our decision-making rather than frightening us. It collapses a lot of the games. When you can’t sell your way out, you have to be right going in.

What actually changes

MOIC over IRR. Without a clock, IRR stops being the right yardstick, and starts becoming misleading. A business that compounds capital at 15% a year for twenty years is an extraordinary outcome that an IRR-optimized model would underweight, because the annualized number looks ordinary next to a quick double. The permanent owner cares about the absolute multiple of capital and the durability of the compounding, not the speed of the round trip.

You pay up for quality. In a flip, entry multiple is your single biggest lever, so price discipline borders on religion. Over a long enough hold, the math inverts. A genuinely great business compounding internally will swamp the entry multiple. The gap between paying 8x and 11x for a business that doubles its earnings every five years is a rounding error two decades out. This is Buffett’s entire evolution: from buying fair businesses at wonderful prices to buying wonderful businesses at fair prices. The permanent owner can afford to overpay for quality and genuinely cannot afford to underpay for mediocrity.

Reinvestment rate becomes the central variable. The cleanest version of compounding is a business that redeploys its own cash internally at high rates of return, so you barely have to do anything. Constellation Software built an entire enterprise on exactly this: buy cash-generative vertical software businesses, then reinvest the cash into more of them at high incremental returns. The underwriting question shifts from “how much cost can we take out” to “how much capital can this business productively absorb, and at what return.” A business with no reinvestment runway (one that can only hand cash back) is worth far less to a permanent owner than one with a long runway, even at the same EBITDA level.

Management succession from day one. In a four-year hold, you can ride a key person; you only need them to last until the sale. Over fifteen or twenty years, that person retires, burns out, or simply isn’t there anymore. The organization has to outlive its best individual. Key-person risk that reads as a strip profile in diligence can become a deal-breaker in permanent capital, so you have to underwrite the second layer on day one: the bench, the systems, the ability to institutionalize what currently lives in one founder’s head. Not as a post-close project, but as a part of the decision to buy.

The trade-offs

What you give up: Leverage. You can’t run flip-level debt on a business you intend to hold through multiple cycles, because you have to survive every one of them, not just exit before the next downturn. Financial engineering and multiple arbitrage disappear as return drivers; the returns have to come from the business itself, which is a much harder place to find them. And the sponsor economics change shape entirely. No carry-crystallizing liquidity event, no big realized mark. Returns accrue through cash flow and compounding, which is less immediately lucrative for the GP and requires a different temperament.

What you get: Compounding. No repeated transaction costs, no taxes triggered on every round trip, no re-underwriting the same dollars over and over again. The deferred tax on unrealized gains is effectively an interest-free loan from the government, and over decades it becomes quite powerful. Real operator alignment, because you’re not quietly prepping the business for sale, which means management isn’t being steered toward a transaction that distorts every incentive along the way. And far less time spent in processes — you’re operating, not perpetually buying in order to sell.

Whether that trade is worth it depends on what you’re optimizing for. If it’s the speed and size of the next realization, permanent capital is not for you. If it’s the terminal value of a business you actually understand, it’s a no-brainer.

The right question

The question stops being “what’s it worth at exit” and starts becoming “what will this business look like in ten years.” That’s admittedly a harder one to answer. There’s no comp set, no buyer appetite to lean on, and no clock to determine value. But it’s also the only question that was ever really worth asking.